15 Min Read

Vlad Zghurskyi

Content Creator

Every cycle has its noise. 2026 just happens to be louder, dumber, and more expensive than most.

15 Min Read

Vlad Zghurskyi

Content Creator

Every cycle has its noise. 2026 just happens to be louder, dumber, and more expensive than most.

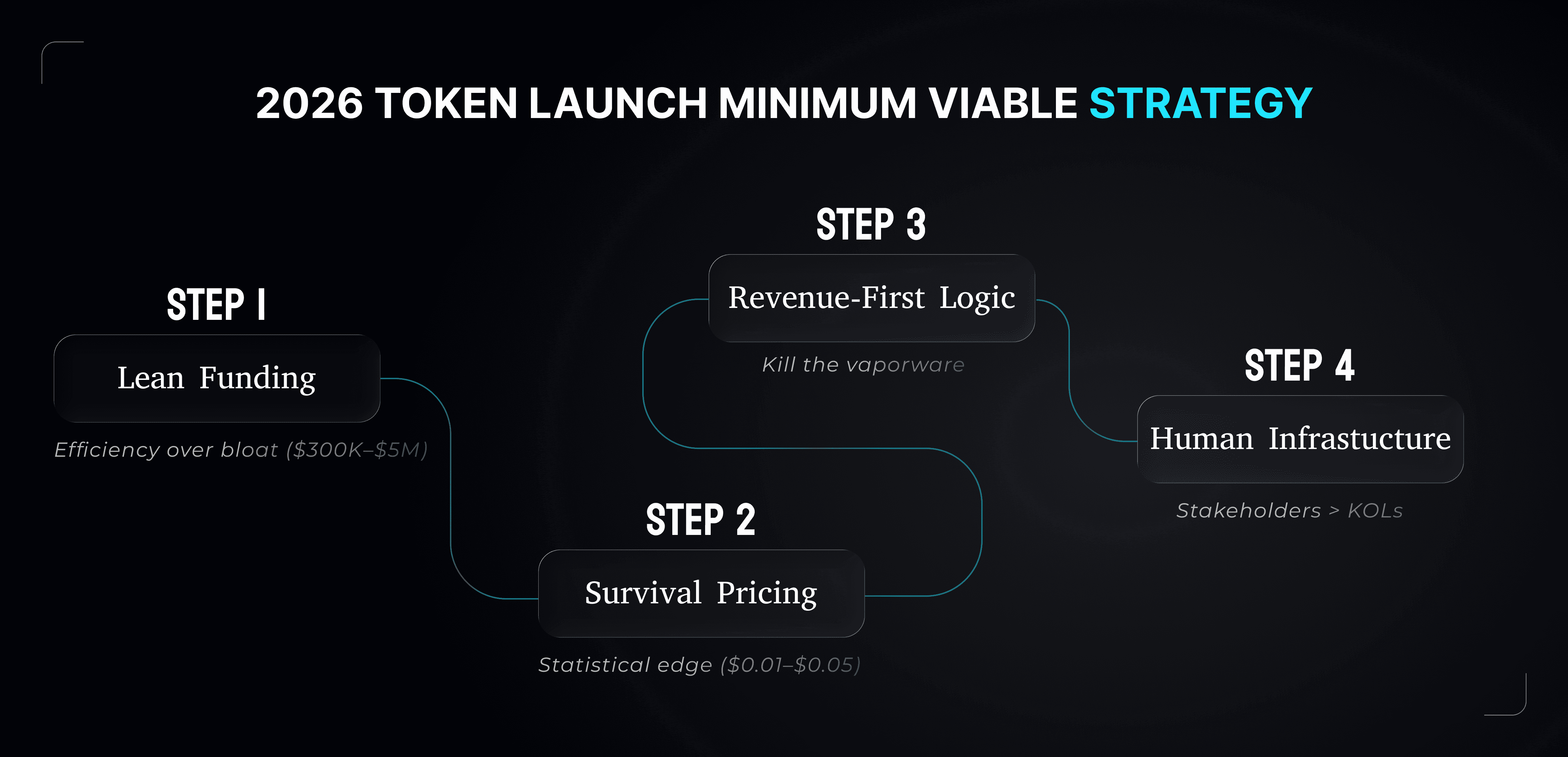

On paper, everything should be working: capital is there, tooling is better, distribution is easier than it’s ever been. And yet, launch after launch is collapsing under its own weight, not six months later or after a bear market. On day one.

That’s not an accident, as you might think, but rather a signal.

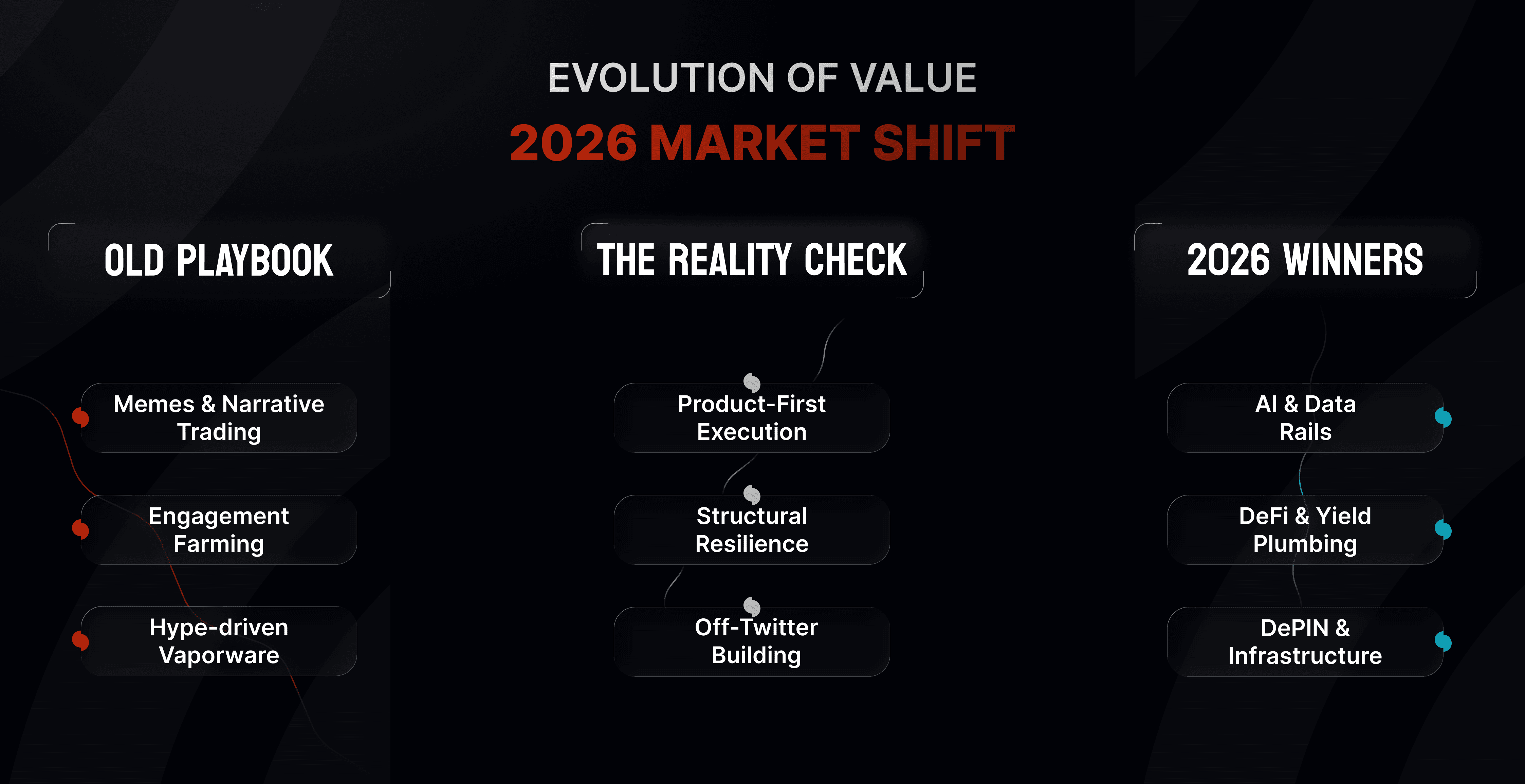

The old playbook (raise big, grow fast, farm engagement, pray for liquidity) has stopped working. The market is not only tired of it. It’s actively punishing it.

And while most teams are still trying to brute-force relevance through noise, a much smaller group is doing the opposite. They’re funded, shipping, and doing their best to solve real infrastructure problems. And they’re doing it quietly, without renting an audience or buying belief.

This article is about those teams.

Before we get into the weeds, here’s the high-level picture.

Solus Growth / Solus Research worked across 30+ TGEs, multiple cycles of Web3. This piece reflects field research.

Disclaimer: This is not investment advice.

There was a time when visibility was a proxy for legitimacy. If everyone was talking about you, surely you were doing something right.

But now, that logic is broken.

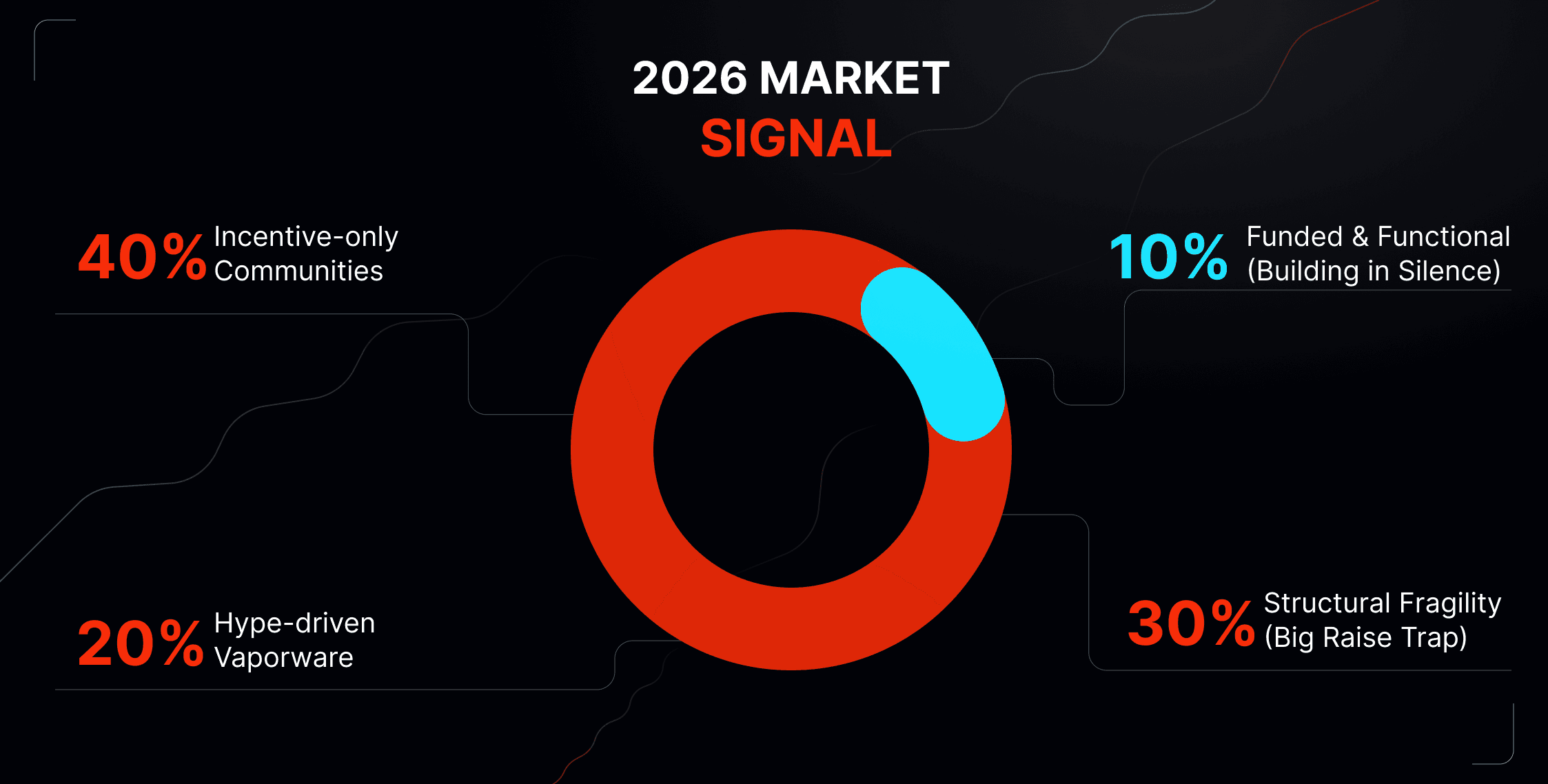

In our December analysis, we broke down 113 token launches - over $1.3B raised - and mapped the single structural pattern behind their failure.

So… Tier-1 funds. Prime exchange listings. Six-figure influencer budgets. And one very consistent outcome: most of them are already dead or walking toward it.

How so?!

The failure mode is not lack of awareness. It’s rather what one might call a “structural fragility”.

Big raises lock teams into growth expectations they can’t sustain. Large communities amplify volatility instead of value. And when your “users” are really just liquidity tourists, the second velocity slows, everything unravels.

The market has matured in one crucial way: it now distinguishes between things that are impressive and things that are necessary.

AI agents need compliance rails, institutions need privacy without regulatory suicide. Payment companies need settlement without pre-funding traps, while capital needs yield without roulette-wheel risk.

These are unavoidable problems.

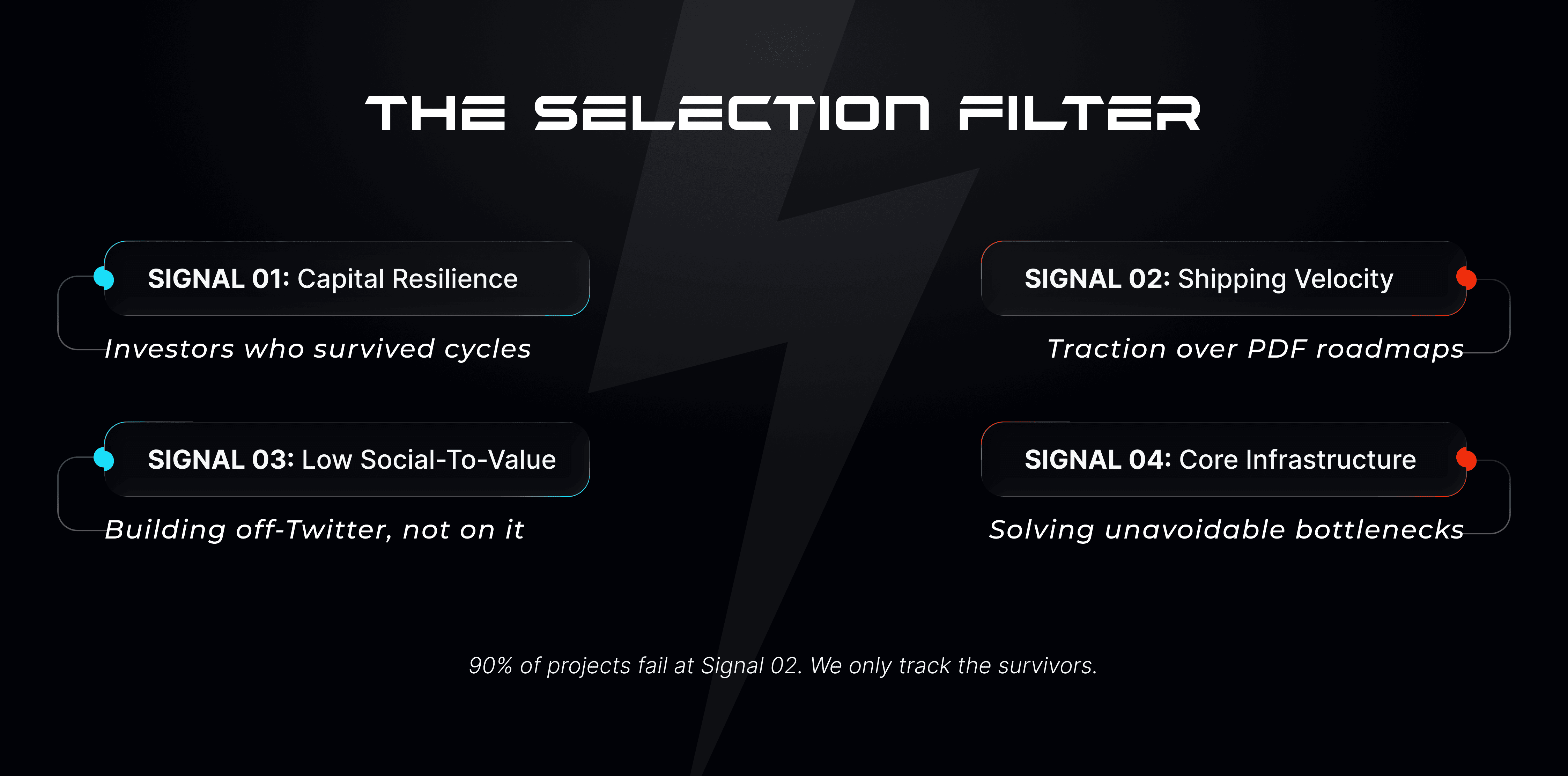

So, how did we choose the ones that should be in the list?

No hype quotas, and no follower minimums. Just fundamentals.

Before throwing twenty names at you, it’s worth understanding where value is actually accumulating. These categories are essentially pressure points.

The AI meme phase is already over. What’s left are systems that need to operate in the real world: legally, autonomously, and at scale.

Web3 is the obvious backend for that, but only if the rails exist.

DeFi is not a casino anymore. It’s becoming financial infrastructure, and infrastructure needs boring things like bonds, credit, and risk management.

The money coming next won’t tolerate directional exposure disguised as innovation.

Radical transparency was useful for bootstrapping. It’s catastrophic for institutions.

At the same time, AI is flooding every open system with synthetic actors. Knowing who is on the other side (without leaking everything about them) is now existential.

Play-to-earn failed because it treated players like extractive resources. The shift to ownership, creators, and real economies is what finally makes gaming work as an onboarding vector.

Centralized infrastructure is efficient—until it breaks. And when it breaks, everything breaks.

DePIN works because incentives scale faster than capex.

The real crypto payment market isn’t in cafés in San Francisco. It’s in regions where legacy rails never worked to begin with.

Velocity beats novelty.

Talk to us

CipherOwl

AI-driven on-chain compliance, backed by a $15M seed co-led by Coinbase Ventures. As regulation tightens, this stops being optional infrastructure and starts becoming table stakes.

Mecka

An $8M-backed data pipeline for robotics and embodied AI. While everyone else trains on text, Mecka is selling the physical context AI actually needs.

Koah

Solving AI’s monetization problem without subscriptions. Ads inside AI conversations sound boring, until you realize this unlocks entire categories of free, scalable AI products.

TomNextAI

Early-stage intelligence infrastructure for private markets. Private assets are opaque, inefficient, and massive. This is the data layer that makes them investable.

Pye Finance

A $5M seed led by Variant and Coinbase Ventures to unlock $59B in illiquid staking capital. Think of it as turning validator lockups into bonds.

Gondor

Credit infrastructure for prediction markets. Borrowing against Polymarket positions didn’t exist six months ago. Now it’s inevitable.

Axis

Institutional delta-neutral yield. Structured products without directional risk. Exactly the kind of boring institutions love.

Block Street

Tokenized stocks with actual liquidity. Not wrappers, markets.

While these teams build in silence, others are using community energy to stay relevant. See which community-focused projects are set to dominate the narrative by 2026.

0xbow.io

Privacy with AML compliance. Integrated into Ethereum Foundation tooling. Backed by Vitalik pre-seed. This is the holy grail for institutional DeFi.

Self Protocol

ZK-based human verification without leaking data. As bots flood the web, this becomes core infrastructure, not a nice-to-have.

Tatakaiio

High-fidelity card RPG backed by gaming-native capital. Ownership at the asset level, not the account level.

Revived

Creator-driven game production from an ex-Minecraft community leader. Mods aren’t an afterthought here, but rather, they’re the economy.

ArgentumAI

GPU allocation and second-life hardware markets. Institutional execution. Sub-500 followers. Massive problem being solved quietly.

Depinsim

Decentralized mobile connectivity via eSIMs. Turning mobile data into a tradable asset is a consumer-facing DePIN wedge that actually makes sense.

AllScale

Crypto-fiat neobank for the unbanked. Zero-gas payments, passkeys, live in Africa, expanding to LatAm. Real PMF territory.

Zynk

“Settle now, pay later” infrastructure. Removing pre-funding constraints unlocks billions in trapped liquidity.

Sprinter

Cross-chain solving as a service. Credit-based liquidity for interoperability that actually scales.

STR8FIRE

Tokenizing Hollywood IP. Culture as an asset class, not just debt instruments with better marketing.

Arx

Secure NFC chips that bind physical objects to on-chain assets. Real-world NFTs that don’t fall apart on contact with reality.

AminoChain

A DeSci L2 for biobanking, backed by a16z. Patients tracking and monetizing biological samples fixes a system legacy institutions never could.

Across all these projects, the same signals keep repeating.

They’re not quiet because they’re lost. They’re quiet because they’re building. Less time on Twitter, more time shipping, integrating, and talking to actual users and partners.

You keep seeing the same names: Coinbase Ventures, a16z, Variant, Robot Ventures. These funds have already been burned by hype. They’re backing teams that can survive, not ones that can trend.

The product works before the token exists. Utility comes first, narrative comes later. The token supports real usage, and it doesn’t exist to explain why the project should matter.

We genuinely want these teams to win. They’ve earned it.

But here is the risk: it would be a tragedy if they focus so strictly on "fundamentals" that they miss the other half of the equation: the token, the narrative, the classic Web3 velocity.

Here’s the thing: Fundamentals alone don’t win in Web3.

This is why we’re already in the trenches with teams like ArgentumAI and STR8FIRE. Execution without distribution is just quiet failure with better intentions.

While we criticize noise, we don’t criticize distribution. The difference matters.

There’s a structural gap between farming impressions and building aligned exposure over time. That’s why long-term KOL infrastructure (not campaign bursts) is becoming critical. Sustainable creator networks, structured ecosystem positioning, and consistent narrative layering are what actually compound.

Most TGEs fail by following the same 45-day post-TGE community crash pattern.

What projects call a “community” is usually 90% airdrop farmers, not future users or advocates.

When community activity collapses, token price collapse is not emotional, but rather mechanical

The real failure lies not in the token itself, but in the absence of any plan for Day 46.

Survivors don’t keep everyone. They shed mercenaries early and retain 20–40% true believers.

A real TGE community retention strategy is designed before launch. It shouldn't be duck-taped later.

Drop us a message

Infrastructure-heavy categories: AI compliance rails, DeFi plumbing, privacy + identity, DePIN, payments/settlement, and real-world assets. These solve unavoidable problems rather than chasing narratives.

Because capital and attention don’t fix structural weaknesses. In 2026, projects without real utility, sustainable token design, and product-market fit collapse quickly, and often right after launch.

Infrastructure-heavy categories: AI compliance rails, DeFi plumbing, privacy + identity, DePIN, payments/settlement, and real-world assets. These solve unavoidable problems rather than chasing narratives.