The stablecoin market has crossed $300 billion and on-chain real-world assets have reached $35.5 billion. Enterprises are reshaping how they settle payments, manage treasury, and deploy working capital. Here is the business case in numbers CFOs can act on.

CONTENT LIST

No sections

First BlackRock launched BUIDL, a tokenized US Treasury fund that now holds $2.85 billion in assets. Then JPMorgan and Morgan Stanley disclosed plans for bank-issued stablecoins and deposit tokens. PayPal launched PYUSD, now at $1.21 billion in market cap. Franklin Templeton put a US government money market fund on Ethereum, Stellar, and Arbitrum. In November 2025, a traditional institutional investor managing more than $25 billion in assets allocated capital to an on-chain Bitcoin yield strategy through Hilbert Group.

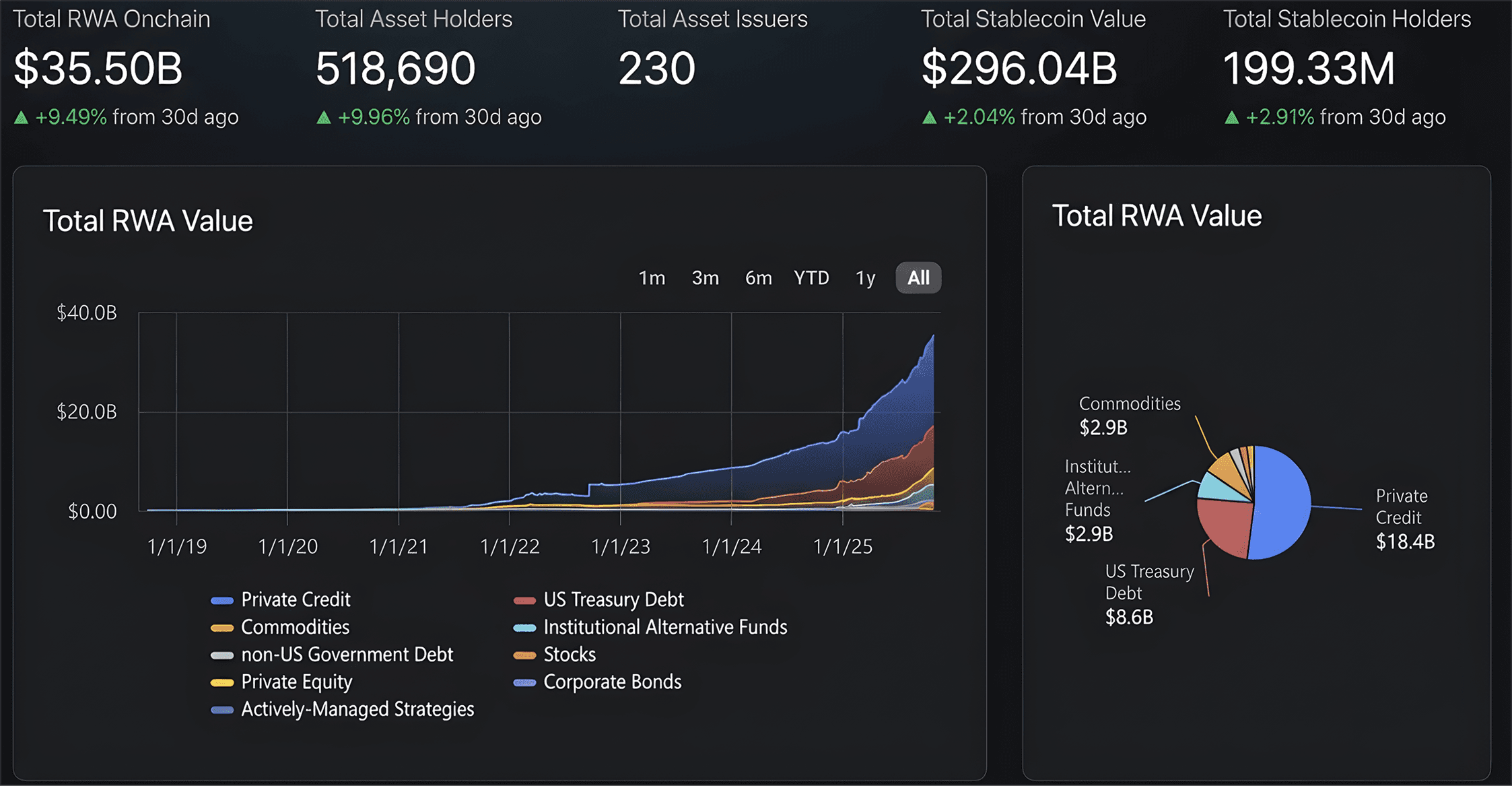

These are not crypto-native firms experimenting at the edges. They are the largest asset managers, banks, and payment networks in the world, moving treasury and payment operations onto blockchain rails. The stablecoin market is now $300 billion, up roughly 75% year-on-year. Total on-chain real-world asset value has reached $35.5 billion, up 118% YTD from $16 billion. Discretionary on-chain investment strategies grew 738% year-to-date in 2025.

For corporate treasurers and CFOs, the question is no longer whether stablecoins and on-chain settlement are legitimate. Regulation, named institutional adoption, and operational data have settled that. The question is which payment corridors in your operation are costing the most, settling the slowest, and locking the most working capital, and whether the on-chain alternative is now mature enough to deliver measurable savings.

The Three Problems Stablecoins Solve for Business

Corporate treasury teams face the same structural friction every quarter: slow cross-border settlement, high correspondent-banking costs, and capital tied up in transit. Stablecoins, cryptocurrencies pegged 1:1 to fiat (typically USD) and backed by liquid reserves such as Treasury bills and cash, address all three. Regulators in the US, EU, Hong Kong, and Singapore have now formalized the rules; the operational case is what remains to evaluate.

Problem 1: Settlement Speed

Cross-border wire transfers typically clear in two to five business days. ACH transactions take one to three days. Both operate within business hours and run through correspondent banking chains that can add additional hops, and additional days, when payment corridors involve multiple jurisdictions.

Settlement on stablecoin rails occurs in seconds, 24 hours a day, seven days a week. For a multinational paying suppliers across time zones, or a fintech reconciling payouts daily, this is a qualitative shift in cash-flow predictability. Capital that would otherwise sit in transit at T+1 or T+2 becomes immediately redeployable, into yield-bearing instruments, supplier prepayments, or other working capital uses.

From days to seconds, 24/7

Traditional cross-border wire: 2–5 business days. ACH: 1–3 days. Stablecoin rails: seconds, with no business-hour or weekend constraints.

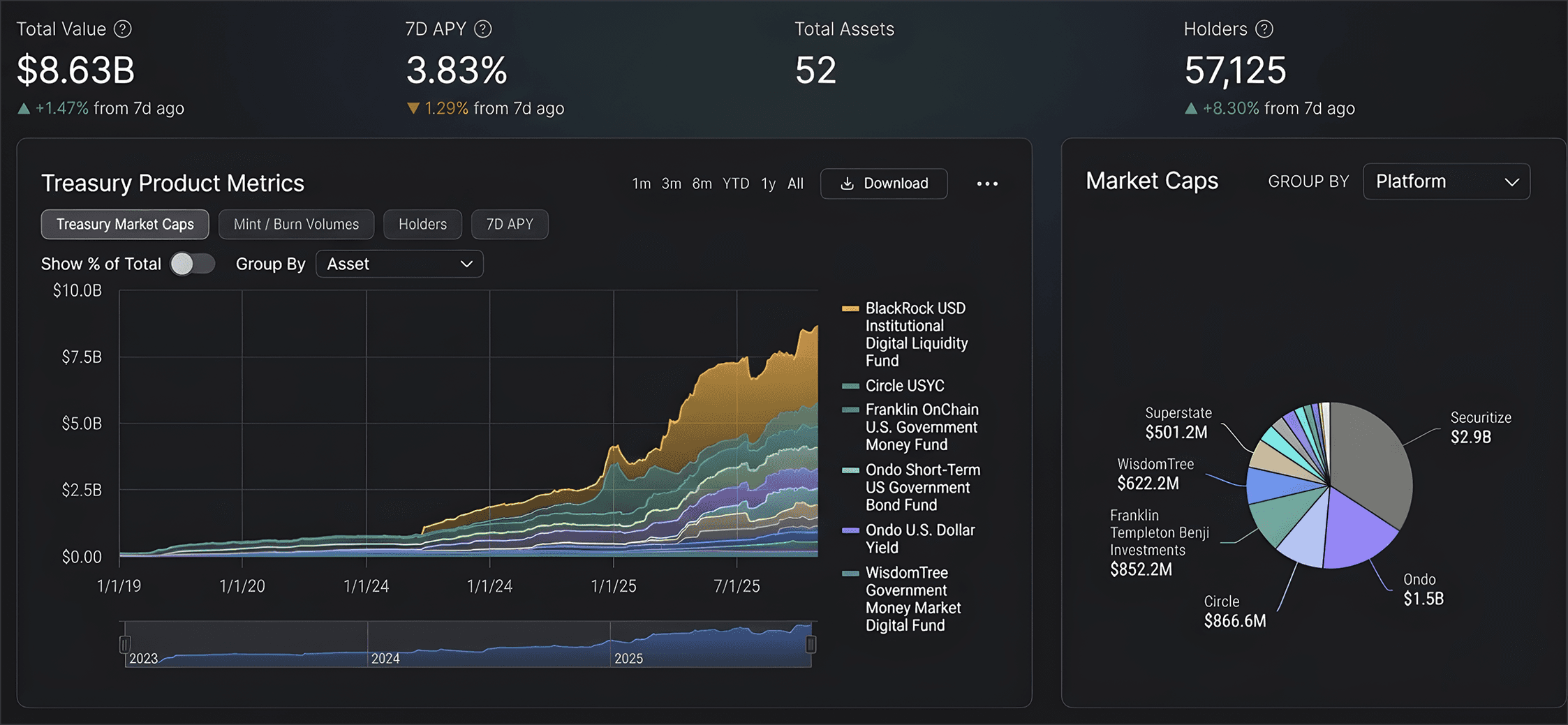

Tokenized US Treasury products reached $8.6B by late 2025, the largest on-chain fixed-income category. BlackRock (BUIDL), Circle (USYC), and Franklin Templeton (BENJI) anchor the market. Source: rwa.xyz.

Problem 2: Cross-Border Cost

The correspondent banking network, the chain of intermediary banks that moves international payments through SWIFT, extracts fees at each hop. A typical cross-border wire carries all-in costs in the low single-digit percentage range when correspondent fees, FX spreads, and intermediary charges are combined. For high-volume payers (importers, platforms disbursing to global contractors, marketplaces handling multi-currency settlements), this is a material line item.

Stablecoin transfers on Layer 2 networks (blockchain scaling solutions such as Base or Arbitrum built on top of Ethereum) cost fractions of a cent per transaction. Value moves directly between counterparties or through the issuer, with no multi-hop fee erosion.

The disintermediation effect is visible at the deposit layer too. Many large-bank stablecoin and dollar-deposit accounts still pay under 1.25%, while DeFi stablecoin deposits on major lending protocols pay roughly 5%. The intermediary margin that traditional banks retain becomes yield that a treasury can capture directly.

5% vs <1.25%

DeFi stablecoin deposit yields on major lending protocols are running near 5%, compared with under 1.25% on most large-bank dollar deposits. The intermediary margin shows up directly in the depositor's yield.

Problem 3: Working Capital Efficiency

Every day that settlement is delayed is a day that working capital, funds available for daily operations, is unavailable. T+1 and T+2 settlement conventions, standard across most traditional payment rails, mean businesses routinely have large sums in operational limbo: sent but not received, or received but not yet cleared.

Instant settlement on stablecoin rails removes that lag. Funds arrive in seconds and become immediately deployable. Beyond pure operational efficiency, enterprises are increasingly using tokenized US Treasury products, on-chain representations of US Treasury bills, for idle stablecoin balances. These products now total more than $8.6 billion across 52 funds and 57,000+ holders. BlackRock's BUIDL, Circle's USYC, Franklin Templeton's BENJI, and Ondo's OUSG pass through Treasury-bill yields of roughly 3.8% to 4.5% annually. Idle stablecoin float can become productive treasury exposure rather than zero-yield cash.

Total on-chain RWA value reached $35.5B with $296B in stablecoin value (late 2025). Private credit ($18.4B) and US Treasury debt ($8.6B) dominate the RWA stack. Source: rwa.xyz.

Table 1: Traditional Rails vs. Stablecoin Rails

Metric

Traditional Rails

Stablecoin Rails

Settlement Speed

2–5 business days (wire), 1–3 days (ACH)

Seconds, 24/7/365

Cross-Border Cost

Low single-digit % (fees + FX spread + intermediaries)

Sub-cent on L2 networks

Operating Hours

Business hours, weekdays only

Always-on, no blackout windows

Working Capital

Capital locked in transit (T+1/T+2)

Immediate redeployment on settlement

Reconciliation

Manual, multi-day

On-chain, near-real-time

Counterparty Chain

Correspondent banking network (multiple hops)

Peer-to-peer or direct issuer

Idle Cash Yield

<1.25% on most bank deposits

~3.8–4.5% via tokenized T-bill products; ~5% on stablecoin lending

Sources: Solus Group analysis; rwa.xyz; public stablecoin issuer disclosures.

Who Is Already Doing This: Named Enterprise Adoption

Institutional adoption of stablecoins and on-chain treasury instruments has moved from pilot to production across banking, payments, and asset management. The organizations below represent the front wave of enterprise integration, and the data is no longer about announcements, it is about live AUM, market cap, and yield.

Banks Issuing Stablecoins and Deposit Tokens

JPMorgan and Morgan Stanley have both disclosed plans for bank-issued stablecoins or deposit tokens, on-chain representations of bank deposits that settle through the issuing institution rather than through a correspondent network. Globally, banks in Hong Kong and the UAE are partnering with fintechs to pilot tokenized deposit systems for institutional clients, with the Central Bank of the UAE overseeing an AED-pegged stablecoin framework.

PayPal's PYUSD, the payment company's USD stablecoin, has reached $1.21 billion in market capitalization, with 97% of reserves in short-term US Treasury bills, operating across both Ethereum and Solana. PayPal's integration of PYUSD into consumer and merchant payments is the largest mainstream corporate deployment of a stablecoin to date.

Asset Managers Operating On-Chain

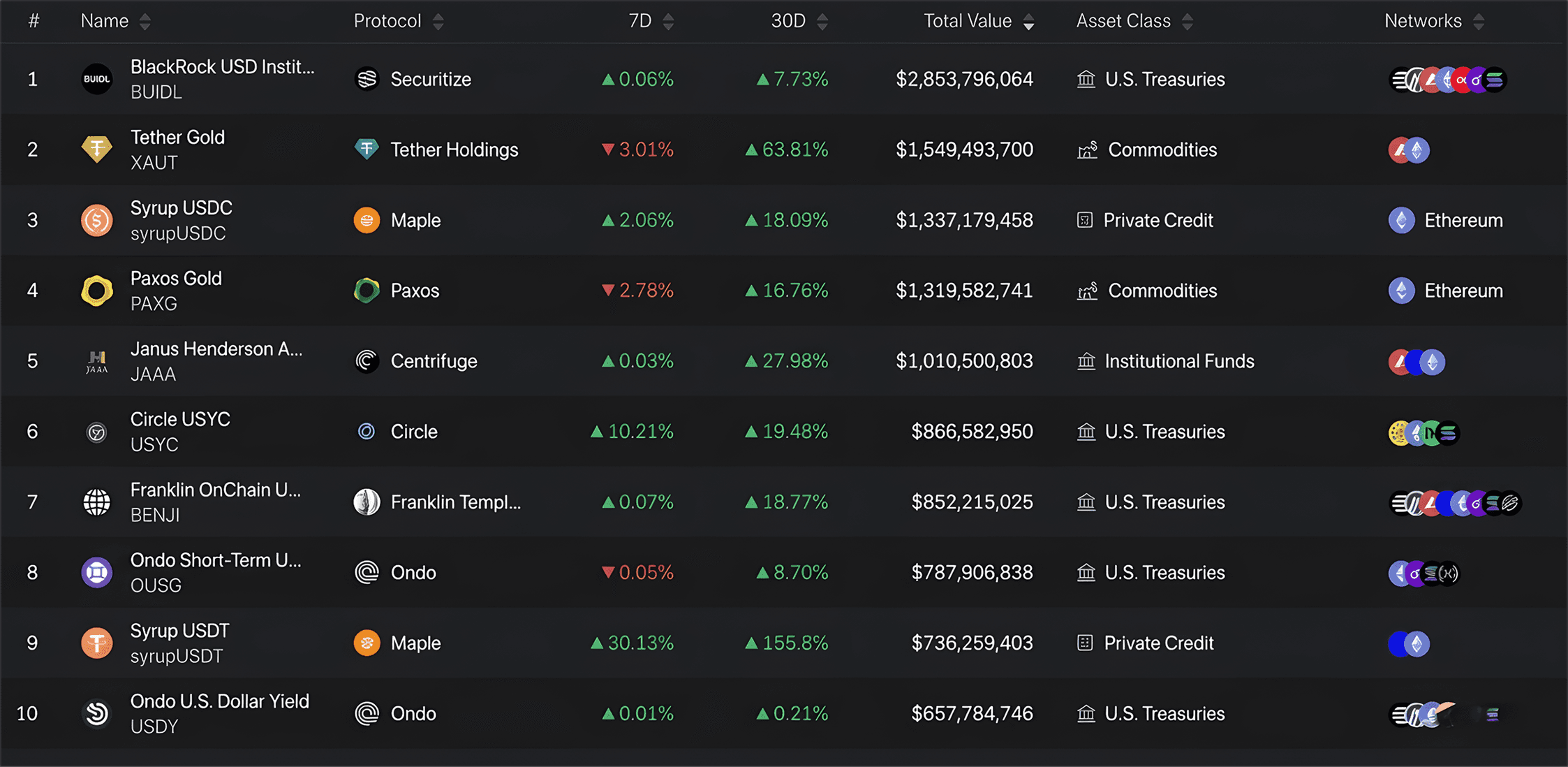

BlackRock's BUIDL (USD Institutional Digital Liquidity Fund) is the clearest signal of asset-manager conviction. Managed via the Securitize platform, BUIDL holds approximately $2.85 billion in AUM, allocates 100% to US Treasury bills, and pays 4.5% APY to permissioned institutional holders. Recent 30-day growth of 7.73% reflects continuing institutional inflows.

Franklin Templeton's BENJI fund, an on-chain US government money market fund, holds ~$852 million across Ethereum, Stellar, and Arbitrum, paying 4.13% APY. Ondo Finance's USDY and OUSG, Circle's USYC, and Janus Henderson's JAAA round out a mature market for institutional on-chain fixed income. Tokenized US Treasury products now span 52 funds serving over 57,000 holders.

Hedge Fund Talent Moving On-Chain

The Keyrock On-Chain Asset Management report shows that discretionary on-chain strategies grew 738% year-to-date in 2025, many of them run by managers who came from traditional hedge funds. The signal is direct: traditional finance talent is following capital onto blockchain rails.

A representative case is Hilbert Group's BTC Basis+ Strategy. In November 2025, Hilbert Group disclosed that a long-term institutional investor managing more than $25 billion in assets had allocated capital to Basis+ via the Hilbert Liberty Fund. The strategy reported +30% USD net and +24% BTC net YTD 2025, with roughly 7% annualized volatility and a Sharpe ratio above 4, a return profile that compares favorably against most TradFi hedge fund mandates, delivered through a regulated fund vehicle rather than direct DeFi interaction.

Top tokenized RWA products by market cap (late 2025). BlackRock BUIDL (~$2.85B) leads tokenized US Treasuries; Maple's Syrup USDC ($1.34B) anchors private credit. Source: rwa.xyz.

Sources: rwa.xyz; public issuer disclosures; Hilbert Group November 2025 update; Solus Group research.

Readytomovefrompilottoproduction?

Benchmarkyourtreasury’son-chainpotential

Benchmarkyourtreasury’son-chainpotential

Book a сall

The Regulatory Green Light

The single most important development enabling corporate treasury adoption is regulatory clarity. Until 2025, compliance officers at most enterprises could not approve stablecoin usage without clear jurisdictional rules. That constraint has been resolved across major financial centers.

United States: GENIUS Act (Signed July 2025)

The GENIUS Act establishes the first comprehensive federal framework for stablecoin issuance in the US. Key provisions: 100% liquid reserves (Treasury bills, cash, or repurchase agreements), monthly public attestations, annual audits, and an explicit classification of stablecoins as payment instruments, not securities and not commodities. This classification matters: it means stablecoins are not subject to securities registration requirements and can be integrated into corporate treasury operations without triggering investment-product compliance obligations.

The framework also recognizes a "Stablecoin-as-a-Service" category, licensed providers enabling institutions to issue or integrate stablecoins without building proprietary technology. The CLARITY Act for broader digital asset markets has also advanced through the legislative process.

European Union: MiCA

The EU's Markets in Crypto-Assets Regulation (MiCA) requires stablecoin issuers operating in Europe to hold Electronic Money Institution (EMI) licensing. An EMI license issued in any EU member state provides a regulatory passport across all 27 EU states, allowing a stablecoin-enabled treasury operation to function across the eurozone under a single compliance framework, analogous to how EMI licensing works for established fintechs.

Asia-Pacific

Hong Kong enacted its Stablecoin Ordinance in May 2025, requiring licensing for fiat-referenced stablecoin issuers operating in or targeting the Hong Kong market. Singapore's Monetary Authority (MAS) refined its digital asset framework in 2025, bringing tokenized securities and stablecoins within the existing securities-law perimeter. The UAE's Central Bank has established an AED-pegged stablecoin framework, positioning the country as a hub for stablecoin-enabled cross-border trade in Gulf markets.

Together, these frameworks mean enterprises with operations in North America, Europe, and Asia-Pacific now have a clear regulatory pathway in each major operating jurisdiction.

EMI licensing; cross-border passport across 27 EU states

Hong Kong

Stablecoin Ordinance

Enacted May 2025

Licensing for fiat-referenced stablecoin issuers; HKMA oversight

Singapore

MAS Framework

Refined 2025

Tokenized securities + stablecoins under existing securities laws

UAE

CBUAE Framework

Active

AED-pegged stablecoin framework; Central Bank oversight

Sources: GENIUS Act (US, July 2025); MiCA (EU); Hong Kong Stablecoin Ordinance (May 2025); MAS Singapore; CBUAE.

Risk Considerations for Enterprise Adoption

CFOs and compliance officers are trained to evaluate risk comprehensively. Any balanced view of on-chain treasury must include a candid assessment of risks alongside operational benefits. There are four primary categories.

Regulatory Risk

Despite the progress above, a jurisdictional patchwork remains. Stablecoins compliant under the US GENIUS Act may carry different reporting obligations under MiCA and different licensing requirements in Asia-Pacific. Enterprises operating globally need jurisdiction-by-jurisdiction analysis before deploying stablecoin treasury operations across an entity structure. Compliance programs must also be built for sustained cadence, monthly attestations, annual audits, ongoing reserve transparency.

Counterparty Risk

Not all stablecoins carry the same risk profile. A stablecoin is only as sound as its issuer's reserve management. Leading issuers publish reserve attestations: USDC holds 46.7% of reserves in US Treasury bills, 43.2% in reverse repo, and the remainder in bank deposits. PayPal's PYUSD holds 97% in short-term Treasury bills. Tether (USDT), while dominant by market cap, maintains a more complex reserve composition that warrants independent assessment. Enterprises should evaluate issuer solvency, reserve quality, and attestation transparency before selecting a primary stablecoin for treasury operations.

Operational Risk

Custody model selection is a critical operational decision. Enterprises must choose between self-custody (managing private keys internally), third-party qualified custodians, or institutional prime brokerage arrangements. Each carries different insurance, liability, and audit-trail characteristics. Smart contract risk, the possibility of vulnerabilities in underlying blockchain code, is reduced but not eliminated by using established protocols. Integration with existing treasury management systems requires technical work and vendor coordination.

Reputational Risk

Board and stakeholder perception of digital assets varies across industries and geographies. Enterprises should prepare governance documentation, audit trails, and compliance evidence before announcing on-chain treasury initiatives. The regulatory frameworks above, GENIUS Act attestations, MiCA audits, provide a ready-made compliance documentation structure that can be presented to auditors, board members, and regulators.

How to Start: A Practical Adoption Roadmap

Enterprise adoption of on-chain treasury does not require a wholesale migration. The most effective approach is a structured pilot that generates measurable data before broader integration. Solus Group recommends a three-phase approach.

Phase 1: Assessment

Map highest-friction payment corridors, routes where settlement speed or cost is most damaging to operations (US–Southeast Asia supplier payments, European payroll for international contractors, etc.).

Calculate current cross-border costs: all-in cost per transaction including correspondent fees, FX spreads, and wire charges. Establish a baseline for the pilot to compare against.

Conduct a regulatory review for each operating jurisdiction the pilot will touch, confirming permitted stablecoin issuers and applicable compliance obligations.

Identify integration points: which treasury management systems, ERP platforms, or payment processors need to connect to on-chain rails.

Phase 2: Pilot

Select a single corridor and a single stablecoin. USDC is the recommended starting point for most enterprises, given its reserve transparency, regulatory engagement, and broad exchange/custodian support. PYUSD may be appropriate for enterprises with significant PayPal payment infrastructure.

Run a controlled pilot at a meaningful but bounded volume, sufficient to generate statistically valid data while contained for operational risk.

Measure three metrics: settlement speed (initiation to confirmed receipt), all-in cost per transaction (including on/off-ramp fees), and reconciliation time. Compare each against your Phase 1 baseline.

Phase 3: Scale

Expand to additional corridors and increase volume based on Phase 2 data. Prioritize corridors where the cost or speed differential is largest.

Integrate stablecoin settlement into the treasury management system. Automate reconciliation. Establish monitoring for on-chain transactions.

Evaluate yield optimization for idle stablecoin balances using tokenized Treasury products (BUIDL, BENJI, USYC, OUSG). On-chain fixed income can generate ~3.8–4.5% annually on cash that would otherwise sit at near-zero rates in a bank current account.

Key Takeaways

Key Takeaways

Key Takeaways

Stablecoins solve three structural treasury problems: settlement speed (seconds vs. days), cross-border cost (fractions of a cent vs. low single-digit %), and working capital efficiency (instant redeployment vs. T+1/T+2 lock-up).

Regulatory clarity is in place across major jurisdictions: US GENIUS Act (July 2025), EU MiCA, Hong Kong Stablecoin Ordinance (May 2025), Singapore MAS, UAE CBUAE framework.

Named enterprise adoption is live and measurable: BlackRock BUIDL ($2.85B), Franklin Templeton BENJI ($852M), PayPal PYUSD ($1.21B), Circle USDC ($66.6B), JPMorgan, Morgan Stanley, Hilbert Group ($25B+ allocator into BTC Basis+).

Discretionary on-chain investment strategies grew 738% YTD in 2025, a direct signal of TradFi talent and capital migrating onto blockchain rails.

Idle stablecoin balances can earn ~3.8–4.5% annually through tokenized Treasury products vs. <1.25% on most bank deposits, turning cash equivalents into productive treasury assets.

A structured three-phase pilot (Assessment → Pilot → Scale) is the recommended entry path. USDC is the preferred starting stablecoin for regulatory clarity and infrastructure breadth.

Stoplosingcapitaltolegacyfriction

Readytomovefrompilottoproduction?

Startyour3-phaseadoptionroadmaptoday

Benchmarkyourtreasury’son-chainpotential

Schedule a call

FAQ

Why are businesses moving funds on-chain?

Three drivers: instant settlement (seconds vs. 2–5-day wires), lower cross-border costs (sub-cent on Layer 2 networks vs. low single-digit percentages on traditional rails), and 24/7 working capital availability. Idle stablecoin balances can also be deployed into tokenized Treasury products yielding roughly 3.8–4.5% annually.

How large is the stablecoin and on-chain RWA market?

The stablecoin market crossed $300 billion in November 2025, up roughly 75% year-on-year. Total on-chain real-world asset value reached $35.5 billion (up 118% YTD from $16 billion), with tokenized US Treasury products alone at $8.6 billion across 52 funds and over 57,000 holders.

Is it legal for businesses to use stablecoins?

Yes, in major financial jurisdictions. The US GENIUS Act (July 2025) explicitly classifies stablecoins as payment instruments, not securities. EU MiCA, the Hong Kong Stablecoin Ordinance (May 2025), Singapore MAS, and the UAE Central Bank framework provide additional regulated structures.

Which named companies already operate on-chain?

BlackRock (BUIDL, $2.85B AUM), Franklin Templeton (BENJI, ~$852M), Circle (USDC, $66.6B), PayPal (PYUSD, $1.21B), JPMorgan (JPM Coin and deposit-token plans), Morgan Stanley (deposit token disclosed), and Hilbert Group (a $25B+ institutional allocator into BTC Basis+ as of November 2025) all operate live on-chain treasury or payment infrastructure.

How do you start moving business funds on-chain?

Start with a single high-friction cross-border corridor. Pilot with USDC (recommended for regulatory clarity), measure settlement speed, all-in cost, and reconciliation time against your traditional baseline, then scale. The full process typically takes 3–6 months with advisory support.

What yields can a treasury earn on idle stablecoin balances?

Tokenized US Treasury products (BUIDL, BENJI, USYC, OUSG) currently pass through approximately 3.8–4.5% annually. Stablecoin lending on major DeFi protocols runs near 5%. By comparison, most large-bank dollar deposits pay under 1.25%.

What are the main risks of on-chain treasury?

Four main categories: regulatory differences across jurisdictions; counterparty risk (varies by stablecoin issuer and reserve composition); operational risk (custody model, smart contract exposure, TMS integration); and reputational risk (board and stakeholder perception). Each is manageable with structured assessment and an experienced advisory partner.